If you’re planning to buy your first home, saving up for all the costs involved can feel daunting, especially when it comes to the down payment.

If you’re planning to buy your first home, saving up for all the costs involved can feel daunting, especially when it comes to the down payment.

![How Changing Mortgage Rates Impact You [INFOGRAPHIC] Simplifying The Market](https://blog.sfloridaluxuryhomes.com/wp-content/uploads/2024/02/How-Changing-Mortgage-Rates-Impact-You-KCM-Share-1.png)

![How Changing Mortgage Rates Impact You [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/KeepingCurrentMatters/content/images/20240222/How-Changing-Mortgage-Rates-Impact-You-KCM-Share.png)

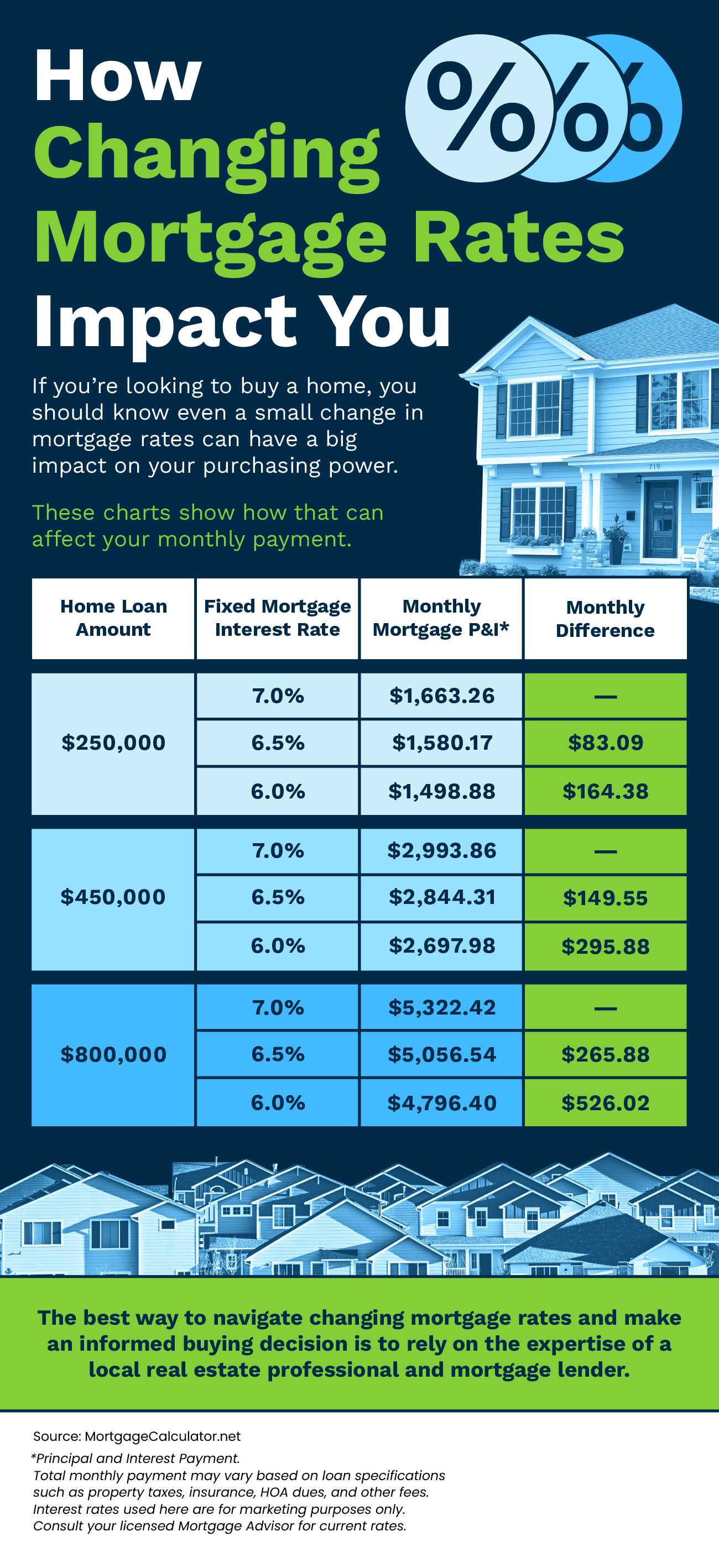

If you’re looking to buy a home, it’s important to know how mortgage rates impact what you can afford and how much you’ll pay each month.

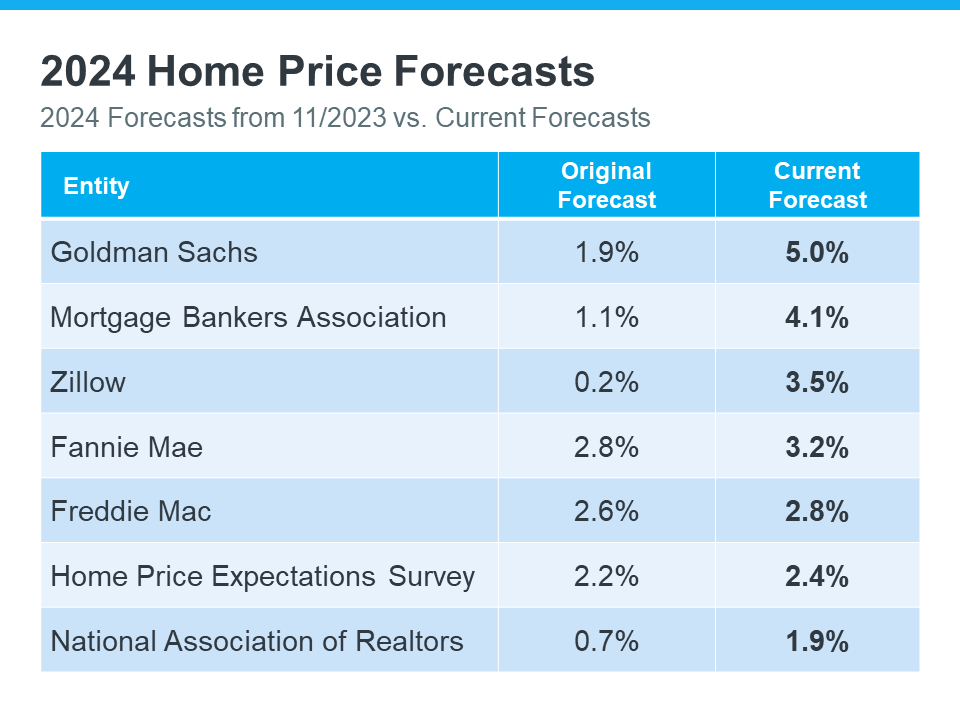

Over the past few months, experts have revised their 2024 home price forecasts based on the latest data and market signals, and they’re even more confident prices will rise, not fall.

So, let’s see exactly how experts’ thinking has shifted – and what’s caused the change.

The chart below shows what seven expert organizations think will happen to home prices in 2024. It compares their first 2024 home price forecasts (made at the end of 2023) with their newest projections:

The middle column shows that, at first, these experts thought home prices would only go up a little this year. But if you look at the column on the right, you’ll see they’ve all updated their forecasts and now think prices will go up more than they originally thought. And some of the differences are major.

There are two big factors keeping such strong upward pressure on home prices. The first is how few homes are for sale right now. According to Business Insider:

“Low home inventory is a chronic problem in the US. This has generally kept home prices up . . .”

A lack of housing inventory has been pushing prices up for a long time now – and that’s not expected to change dramatically this year. But what has changed a bit is mortgage rates.

Late last year when most housing market experts were calling for home prices to rise only a little bit in 2024, mortgage rates were up and buyer demand was more moderate.

Now that rates have come down from their peak last October, and with further declines expected over the course of the year, buyer demand has picked up. That increase in demand, along with an ongoing lack of inventory, is what’s caused the experts to feel the upward pressure on prices will be stronger than they expected a couple months ago.

Real estate experts regularly revise their home price forecasts as the housing market shifts. It’s a normal part of their job that ensures their projections are always up-to-date and factor in the latest changes in the housing market.

That means they’ll continue to revise their projections as the housing market changes, just as they’ve always done. How those forecasts change next is anyone’s guess, but pay attention to mortgage rates.

If they trend down as the year goes on, as they’re expected to do, that could lead to more buyer demand and even higher home price forecasts.

Basically, it’s all about supply and demand. With supply still so limited, anything that causes demand to go up will likely cause prices to go up, too.

At first, experts believed home prices would only go up a little this year. But now, they’ve changed their minds and forecast prices will grow even more than they originally thought. Connect with a local real estate agent so you know what to expect with prices in your area.

Over the past few months, experts have revised their 2024 home price forecasts based on the latest data and market signals, and they’re even more confident prices will rise, not fall.

There’s a lot of confusion in the market about what’s happening with day-to-day movement in mortgage rates right now, but here’s what you really need to know: compared to the near 8% peak last fall, mortgage rates have trended down overall.

And if you’re looking to buy or sell a home, this is a big deal. While they’re going to continue to bounce around a bit based on various economic drivers (like inflation and reactions to the consumer price index, or CPI), don’t let the short-term volatility distract you. The experts agree the overarching downward trend should continue this year.

While we won’t see the record-low rates homebuyers got during the pandemic, some experts think we should see rates dip below 6% later this year. As Dean Baker, Senior Economist, Center for Economic Research, says:

“They will almost certainly not fall to pandemic lows, although we may soon see rates under 6.0 percent, which would be low by pre-Great Recession standards.”

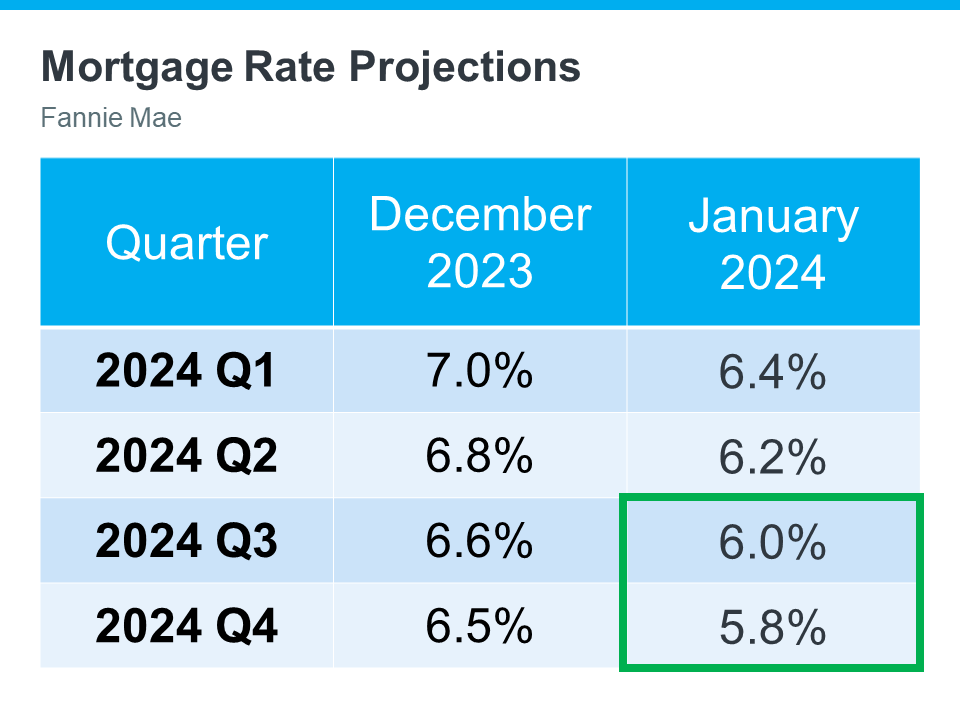

And Baker isn’t the only one saying this is a possibility. The latest Fannie Mae projections also indicate we may see a rate below 6% by the end of this year (see the green box in the chart below):

The chart shows mortgage rate projections for 2024 from Fannie Mae. It includes the one that came out in December, and compares it to the updated 2024 forecast they released just one month later. And if you look closely, you’ll notice the projections are on the way down.

It’s normal for experts to re-forecast as they watch current market trends and the broader economy, but what this shows is experts are feeling confident rates should continue to decline, if inflation cools.

But remember, no one can say for sure what will happen (and by when) – and short-term volatility is to be expected. So, don’t let small fluctuations scare you. Focus on the bigger picture.

If you’ve found a home you love in today’s market – especially where finding a home that meets your budget and your needs can be a challenge – it’s probably not a good idea to try to time the market and wait until rates drop below 6%.

With rates already lower than they were last fall, you have an opportunity in front of you right now. That’s because even a small quarter point dip in rates gives your purchasing power a boost.

If you wanted to move last year but were holding off hoping rates would fall, now may be the time to act. Connect with a real estate agent to get the ball rolling.

There’s a lot of confusion in the market about what’s happening with day-to-day movement in mortgage rates right now.

Buying your first home is a big, exciting step and a major milestone that has the power to improve your life. As a first-time homebuyer, it’s a dream you can make come true, but there are some hurdles you’ll need to overcome in today’s housing market – specifically the limited supply of homes for sale and ongoing affordability challenges.

So, if you’re ready, willing, and able to buy your first home, here are three tips to help you turn your dream into a reality.

Paying the initial costs of homeownership, like your down payment and closing costs, can feel a bit daunting. But there are many assistance programs for first-time homebuyers that can help you get a loan with little or no money upfront. According to Bankrate:

“. . . you might qualify for a first-time homebuyer loan or assistance. First-time buyer loans typically have more flexible requirements, such as a lower down payment and credit score. Many help buyers with closing costs and the down payment through grants and low-interest loans.”

To find out more, talk to your state’s housing authority or check out websites like Down Payment Resource.

Right now, there aren’t enough homes for sale for everyone who wants to buy one. That’s pushing home prices up and making affordability tight for buyers. One way to deal with that issue and find a home right now is to consider condos and townhomes. Realtor.com explains:

“For many newbies, it might just be a matter of making a shift toward something they can better afford—like a condo or townhome. These lower-cost homes have historically been a stepping stone for buyers looking for a less expensive alternative to a single-family home.”

One reason why they may be more affordable is because they’re often smaller. But they still give you the chance to get your foot in the door and achieve your goal of owning a home and building equity. And that equity can help fuel your move into a larger home later on if you decide you need something bigger in the future. Hannah Jones, Senior Economic Analyst at Realtor.com, says:

“Condos can help prospective homebuyers who perhaps have a smaller budget, but who are really determined to get a foothold in the market and start to accumulate some equity. It can be a really great entry point.”

Another way to break into the market is by purchasing a home with friends or loved ones. That way you can split the cost of things like the mortgage and bills, to make it easier to afford a home. According to Money.com:

“Buying a home with another person has some obvious advantages in the mortgage department. With two incomes in the mix, buyers can likely qualify for a larger mortgage — a big help in today’s high-cost market.”

By exploring first-time homebuyer assistance, condos, townhomes, and multi-generational living, it can be easier to find and buy your first home. When you’re ready, connect with a local real estate agent.

Buying your first home is a big, exciting step and a major milestone that has the power to improve your life.

If you’re thinking of selling your house this spring, now is the perfect time to start getting it ready.