Thinking about buying a home?

Thinking about buying a home?

Thinking about buying a home?

The number of homes for sale is playing a big role in today’s housing market.

Thinking about selling your house?

Thinking about selling your house?

![Equity Can Make Your Move Possible When Affordability Is Tight [INFOGRAPHIC] | Keeping Current Matters](https://blog.sfloridaluxuryhomes.com/wp-content/uploads/2024/04/Equity-Can-Make-Your-Move-Possible-When-Affordability-Is-Tight-KCM-Share-3.png)

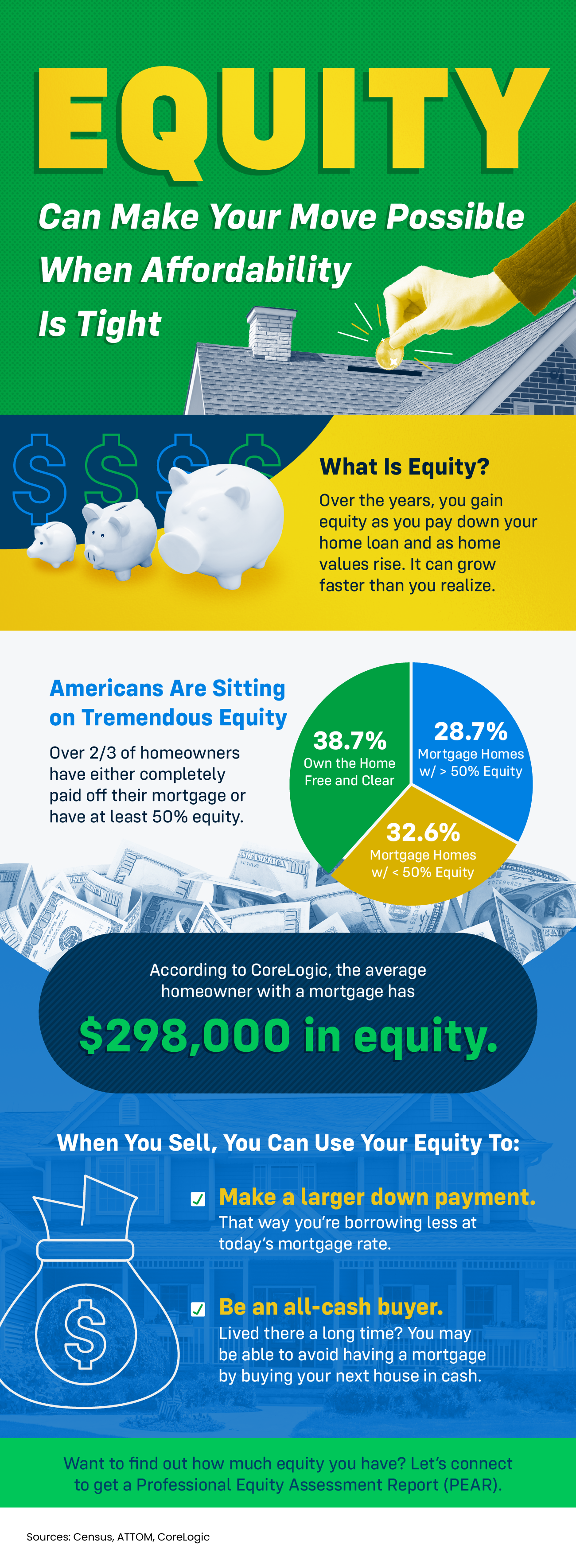

Did you know the equity you have in your current house can help make your move possible?

![Equity Can Make Your Move Possible When Affordability Is Tight [INFOGRAPHIC] | Keeping Current Matters](https://files.keepingcurrentmatters.com/KeepingCurrentMatters/content/images/20240424/Equity-Can-Make-Your-Move-Possible-When-Affordability-Is-Tight-KCM-Share.png)

Did you know the equity you have in your current house can help make your move possible?

![Equity Can Make Your Move Possible When Affordability Is Tight [INFOGRAPHIC] Simplifying The Market](https://blog.sfloridaluxuryhomes.com/wp-content/uploads/2024/04/Equity-Can-Make-Your-Move-Possible-When-Affordability-Is-Tight-KCM-Share-1.png)

Did you know the equity you have in your current house can help make your move possible?

Ever thought about living in the same house with your grandparents, parents, or other loved ones?