It’s clear that consumers are concerned about how quickly home values are rising. Many people fear the speed of appreciation may lead to a crash in prices later this year. In fact, Google reports that the search for “When is the housing market going to crash?” has actually spiked 2450% over the past month.

In addition, Jim Dalrymple II of Inman News notes:

“One of the most noteworthy things that came up in Inman’s conversations with agents was that every single one said they’ve had conversations with clients about whether or not the market is heading into a bubble.”

To alleviate some of these concerns, let’s look at what several financial analysts are saying about the current residential real estate market. Within the last thirty days, four of the major financial services giants came to the same conclusion: the housing market is strong, and price appreciation will continue. Here are their statements on the issue:

Goldman Sachs’ Research Note on Housing:

“Strong demand for housing looks sustainable. Even before the pandemic, demographic tailwinds and historically-low mortgage rates had pushed demand to high levels. … consumer surveys indicate that household buying intentions are now the highest in 20 years. … As a result, the model projects double-digit price gains both this year and next.”

Joe Seydl, Senior Markets Economist, J.P.Morgan:

“Homebuyers—interest rates are still historically low, though they are inching up. Housing prices have spiked during the last six-to-nine months, but we don’t expect them to fall soon, and we believe they are more likely to keep rising. If you are looking to purchase a new home, conditions now may be better than 12 months hence.”

Morgan Stanley, Thoughts on the Market Podcast:

“Unlike 15 years ago, the euphoria in today’s home prices comes down to the simple logic of supply and demand. And we at Morgan Stanley conclude that this time the sector is on a sustainably, sturdy foundation . . . . This robust demand and highly challenged supply, along with tight mortgage lending standards, may continue to bode well for home prices. Higher interest rates and post pandemic moves could likely slow the pace of appreciation, but the upward trajectory remains very much on course.”

Merrill Lynch’s Capital Market Outlook:

“There are reasons to believe that this is likely to be an unusually long and strong housing expansion. Demand is very strong because the biggest demographic cohort in history is moving through the household-formation and peak home-buying stages of its life cycle. Coronavirus-related preference changes have also sharply boosted home buying demand. At the same time, supply is unusually tight, with available homes for sale at record-low levels. Double-digit price gains are rationing the supply.”

Bottom Line

If you’re concerned about making the decision to buy or sell right now, let’s connect to discuss what’s happening in our local market.

Content previously posted on Keeping Current Matters

It’s clear that consumers are concerned about how quickly home values are rising. Many people fear the speed of appreciation may lead to a crash in prices later this year. In fact, Google reports that the search for “When is the housing market going to crash?” has actually spiked 2450% over the past month. In […]

It’s clear that consumers are concerned about how quickly home values are rising. Many people fear the speed of appreciation may lead to a crash in prices later this year. In fact, Google reports that the search for “When is the housing market going to crash?” has actually spiked 2450% over the past month. In […]

There’s no doubt that 2021 is the year of the seller when it comes to the housing market. If you’re a homeowner thinking of moving to better suit your changing needs, now is the perfect time to do so. Low mortgage rates are in your favor when you’re ready to purchase your dream home, and […]

There’s no doubt that 2021 is the year of the seller when it comes to the housing market. If you’re a homeowner thinking of moving to better suit your changing needs, now is the perfect time to do so. Low mortgage rates are in your favor when you’re ready to purchase your dream home, and […]![The Power of Mortgage Pre-Approval [INFOGRAPHIC] | Simplifying The Market](https://blog.sfloridaluxuryhomes.com/wp-content/uploads/2021/05/20210507-KCM-Share-549x300-2.png)

![The Power of Mortgage Pre-Approval [INFOGRAPHIC] | Simplifying The Market](https://blog.sfloridaluxuryhomes.com/wp-content/uploads/2021/05/20210507-MEM-1.png)

![The Power of Mortgage Pre-Approval [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/05/06093846/20210507-KCM-Share-549x300.png)

Many people are sitting on the fence trying to decide if now’s the time to buy a home. Some are renters who have a strong desire to become homeowners but are unsure if buying right now makes sense. Others may be homeowners who are realizing that their current home no longer fits their changing needs. […]

Many people are sitting on the fence trying to decide if now’s the time to buy a home. Some are renters who have a strong desire to become homeowners but are unsure if buying right now makes sense. Others may be homeowners who are realizing that their current home no longer fits their changing needs. […]

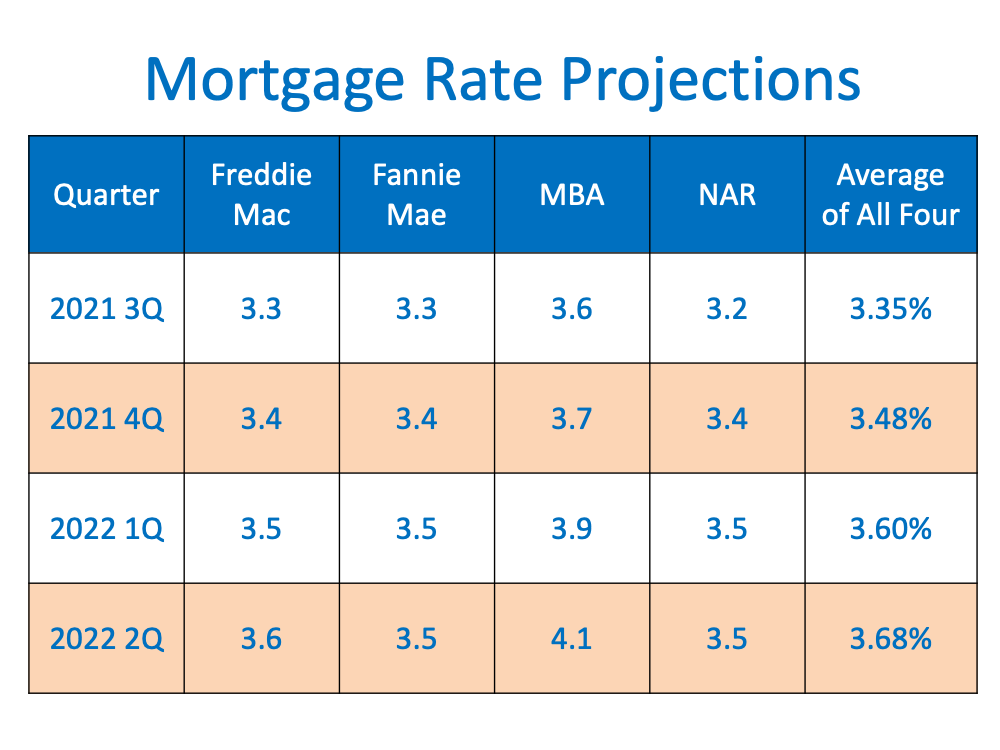

So far this year, mortgage rates continue to hover around 3%, encouraging many hopeful homebuyers to enter the housing market. However, there’s a good chance rates will increase later this year and going into 2022, ultimately making it more expensive to borrow money for a home loan. Here’s a look at what several experts have […]

So far this year, mortgage rates continue to hover around 3%, encouraging many hopeful homebuyers to enter the housing market. However, there’s a good chance rates will increase later this year and going into 2022, ultimately making it more expensive to borrow money for a home loan. Here’s a look at what several experts have […]