Have you been saving up to buy a home this year?

Have you been saving up to buy a home this year?

Have you been saving up to buy a home this year? If so, you know there are a number of expenses involved – from your down payment to closing costs. But did you also know your tax refund can help you pay for some of these expenses? As Credit Karma explains:

“If one of your goals is to stop renting and buy a home, you’ll need to save up for closing costs and a down payment on the mortgage. A tax refund can give you a start on the road to homeownership. If you’ve already started to save, your tax refund could move you down the road faster.”

While how much money you may get in a tax refund is going to vary, it can be encouraging to have a general idea of what’s possible. Here’s what CNET has to say about the average increase people are seeing this year:

“The average refund size is up by 6.1%, from $2,903 for 2023’s tax season through March 24, to $3,081 for this season through March 22.”

Sounds great, right? Remember, your number is going to be different. But if you do get a refund, here are a few examples of how you can use it when buying a home. According to Freddie Mac:

The best way to get ready to buy a home is to work with a team of trusted real estate professionals who understand the process and what you’ll need to do to be ready to buy.

Your tax refund can help you reach your savings goal for buying a home. Connect with a local real estate professional about what you’re looking for, because your home may be more within reach than you think.

According to recent data from Fannie Mae, almost 1 in 4 people still think home prices are going to come down. If you’re one of the people worried about that, here’s what you need to know.

A lot of that fear is probably coming from what you’re hearing in the media or reading online. But here’s the thing to remember. Negative news sells. That means, you may not be getting the full picture. You may only be getting the clickbait version. As Jay Thompson, a Real Estate Industry Consultant, explains:

“Housing market headlines are everywhere. Many are quite sensational, ending with exclamation points or predicting impending doom for the industry. Clickbait, the sensationalizing of headlines and content, has been an issue since the dawn of the internet, and housing news is not immune to it.”

Here’s a look at the data to set the record straight.

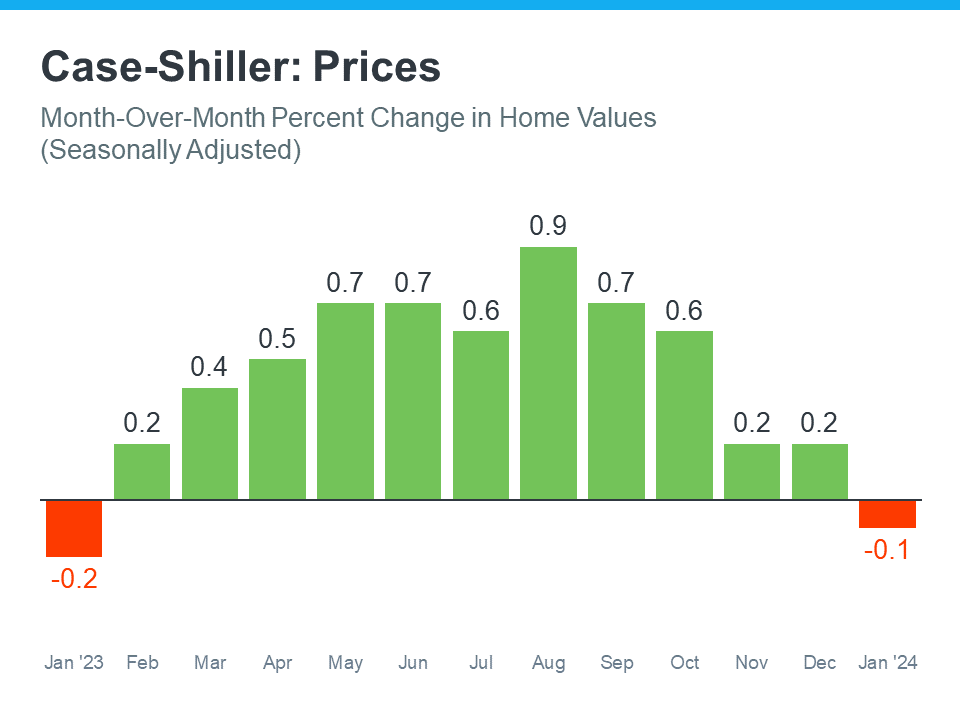

Case-Shiller releases a report each month on the percent of monthly home price changes. If you look at their data from January 2023 through the latest numbers available, here’s what you’d see:

What do you notice when you look at this graph? It depends on what color you’re more drawn to. If you look at the green, you’ll see home prices rose for the majority of the past year.

But, if you’re drawn to the red, you may only focus on the two slight declines. This is what a lot of media coverage does. Since negative news sells, drawing attention to these slight dips happens often. But that loses sight of the bigger picture.

Here’s what this data really says. There’s a lot more green in that graph than red. And even for the two red bars, they’re so slight, they’re practically flat. If you look at the year as a whole, home prices still rose overall.

It’s perfectly normal in the housing market for home price growth to slow down in the winter. That’s because fewer people move during the holidays and at the start of the year, so there’s not as much upward pressure on home prices during that time. That’s why, even the green bars toward the end of the year show smaller price gains.

To sum all that up, the source for that data in the graph above, Case Shiller, explains it like this:

“Month-over-month numbers were relatively flat, . . . However, the annual growth was more significant for both indices, rising 7.4 percent and 6.6 percent, respectively.”

If one of the expert organizations tracking home price trends says the very slight dips are nothing to worry about, why be concerned? Even Case-Shiller is drawing your attention to how those were virtually flat and how home prices actually grew over the year.

Don’t let what you’re hearing about home prices confuse you. The data shows that, as a whole, home prices rose over the past year. If you have questions about what’s happening with home prices in your local area, connect with a trusted real estate professional.

According to recent data from Fannie Mae, almost 1 in 4 people still think home prices are going to come down.

Have you been saving up to buy a home this year?

![The Perks of Downsizing When You Retire [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/KeepingCurrentMatters/content/images/20240408/The-Perks-of-Downsizing-When-You-Retire-KCM-Share.png)

If you’re about to retire, or just did, downsizing can be a good way to try to cut down on some of your expenses.

When mortgage rates spiked up over the last few years, some homeowners put their plans to move on pause.

You may have heard headlines in the news lately about agents in the real estate industry and discussions about their commissions. And if you’re following along, it can be pretty confusing. But here’s the thing you really need to know – expert advice from a trusted real estate agent is priceless, now more than ever. And here’s why.

A real estate agent does a lot more than you may realize.

Your agent is the person who will guide you through every step when buying a home and look out for your best interests along the way. They smooth out a complex process and take away the bulk of the stress of what’s likely your largest purchase ever. And that’s exactly what you want and deserve.

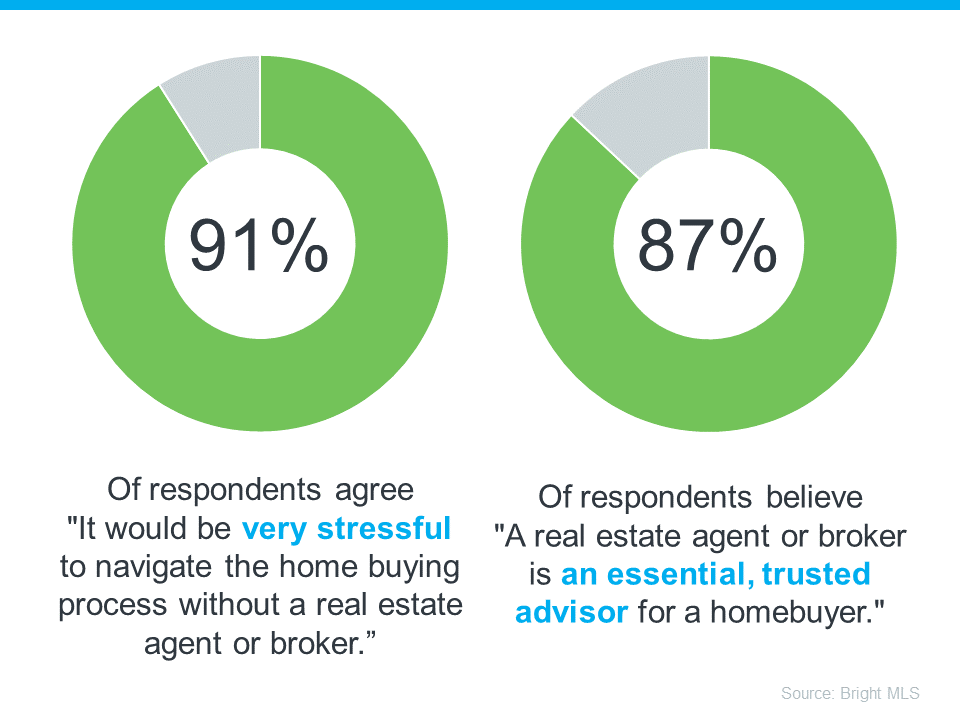

This is at least a part of the reason why a recent survey from Bright MLS found an overwhelming majority of people agree an agent is a key part of the homebuying process (see visual below):

To give you a better idea of just a few of the top ways agents add value, check out this list.

The right agent – the professional – will coach you through everything from start to finish. With professional training and expertise, agents know the ins and outs of the buying process. And in today’s complex market, the way real estate transactions are executed is constantly changing, so having the best advice on your side is essential.

In a world that’s powered by data, a great agent can clarify what it all means, separate fact from fiction, and help you understand how current market trends apply to your unique search. From how quickly homes are selling to the latest listings you don’t want to miss, they can explain what’s happening in your specific local market so you can make a confident decision.

Agents help you understand the latest pricing trends in your area. What’s a home valued at in your market? What should you think about when you’re making an offer? Is this a house that might have issues you can’t see on the surface? No one wants to overpay, so having an expert who really gets true market value for individual neighborhoods is priceless. An offer that’s both fair and competitive in today’s housing market is essential, and a local expert knows how to help you hit the mark.

In a fast-moving and heavily regulated process, agents help you make sense of the necessary disclosures and documents, so you know what you’re signing. Having a professional that’s trained to explain the details could make or break your transaction, and is certainly something you don’t want to try to figure out on your own.

From offer to counteroffer and inspection to closing, there are a lot of stakeholders involved in a real estate transaction. Having someone on your side who knows you and the process makes a world of difference. An agent will advocate for you as they work with each party. It’s a big deal, and you need a partner at every turn to land the best possible outcome.

Real estate agents are specialists, educators, and negotiators. They adjust to market changes and keep you informed. And keep in mind, every time you make a big decision in your life, especially a financial one, you need an expert on your side.

Expert advice from a trusted professional is priceless. Connect with a local real estate agent today.

You may have heard headlines in the news lately about agents in the real estate industry and discussions about their commissions.

If you have student loans and want to buy a home, you might have questions about how your debt affects your plans. Do you have to wait until you’ve paid off those loans before you can buy your first home? Or is it possible you could still qualify for a home loan even with that debt? Here’s a look at the latest information so you have the answers you need.

A Bankrate article explains:

“Roughly 60 percent of U.S. adults who have held student loan debt have put off making important financial decisions due to that debt . . . For Gen Z and millennial borrowers alone, that number rises to 70 percent.”

This includes one of the biggest financial decisions you’ll ever make, buying a home. But you should know, even with student loans, waiting to buy a home may not be necessary. While everyone’s situation is unique, your goal may be more within your reach than you realize. Here’s why.

According to an annual report from the National Association of Realtors (NAR), 38% of first-time buyers had student loan debt and the typical amount was $30,000.

That means other people in a similar situation were able to qualify for and buy a home even though they also had student loans. And you may be able to do the same, especially if you have a steady source of income. As an article from Bankrate says:

“. . . you can have student loans and a mortgage at the same time. . . . If you have student loans and want a mortgage, there are multiple home loan programs you might qualify for . . .”

The key takeaway is, for many people, homeownership is achievable even with student loans.

You don’t have to figure this out on your own. The best way to make a decision about your goals and next steps is to talk to the professionals. A trusted lender can walk you through your options based on your situation, and share what’s worked for other buyers.

Lots of other people with student loan debt are able to buy their own homes. Talk to a lender to go over your options and see how close you are to reaching your goal.